Imagine you’re trying to keep track of your finances, but instead of a single, trusty notebook, you share identical notebooks with everyone in your friend group. Each time someone buys a coffee or lends money, they all write it down in their notebook. Sound complicated? Welcome to the wonderful, mysterious, and surprisingly logical world of blockchain!

Blockchain technology has revolutionized how we think about security, transparency, and trust in the digital age. But if you’ve ever found yourself nodding along in conversations about “blocks” and “chains” without a clue, you’re not alone. Let’s break it down step by step—no tech degree required.

What Is Blockchain?

At its core, a blockchain is a digital ledger. Think of it as a high-tech spreadsheet that records transactions. But here’s the twist: instead of storing that spreadsheet on one computer, it’s spread across a vast network of computers (called nodes).

- Why a chain? Because it links blocks of information (transactions) together chronologically.

- Why so secure? Every block is verified by multiple nodes before it joins the chain, making it nearly tamper-proof.

Blockchain isn’t just for Bitcoin anymore. It powers everything from supply chains to voting systems, but its fundamentals remain the same. Let’s dive deeper.

Step 1: The Birth of a Block

When someone initiates a transaction (let’s say Alice pays Bob 5 Bitcoin), it doesn’t immediately get added to the blockchain. First, it needs to be verified and grouped with other transactions to form a block.

Each block contains:

- Transaction Data – Information about the transaction (e.g., sender, receiver, amount).

- Timestamp – When the block was created.

- Previous Block Hash – A unique code linking it to the previous block.

- Current Block Hash – A code representing the current block.

This combination of data makes it easy to track everything back to the beginning of the chain.

Step 2: Verification – Trust, But Verify

Here’s where things get clever. Transactions are verified by the network of nodes using a consensus mechanism. This ensures everyone agrees the transaction is legitimate. There are several ways to achieve consensus:

Proof of Work (PoW)

- How it works: Miners (powerful computers) solve complex mathematical puzzles to validate a block.

- Reward: Successful miners earn cryptocurrency.

- Downside: Energy-intensive and slow.

Proof of Stake (PoS)

- How it works: Validators are chosen based on the number of coins they hold (their “stake”).

- Reward: Validators earn fees, not new coins.

- Upside: More energy-efficient and faster than PoW.

Other mechanisms like Proof of Authority and Delegated Proof of Stake add even more variety, but they all share the same goal: ensuring consensus.

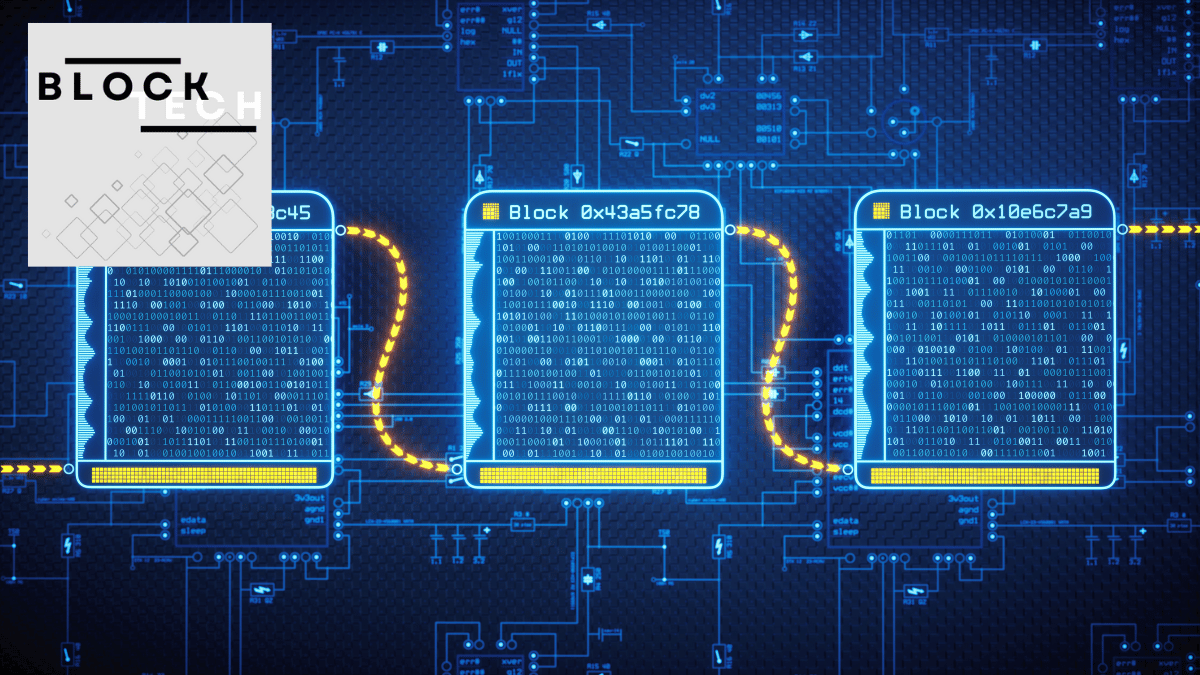

Step 3: Linking the Blocks

Once a block is verified, it’s added to the chain. But here’s the catch: every block is connected via its hash.

A hash is like a digital fingerprint. It’s unique, unchangeable, and derived from the block’s data. If someone tries to alter even a tiny piece of information (like changing “5 Bitcoin” to “50 Bitcoin”), the hash changes, alerting the network that something fishy is happening.

Step 4: Distributed and Decentralized

One of blockchain’s superpowers is decentralization. Instead of storing data on one server (a hacker’s dream), blockchain stores it across multiple nodes.

Why is this important?

- No single point of failure. If one node goes down, the others keep the system running.

- Hard to hack. Altering a single block would require hacking every node simultaneously—a nearly impossible feat.

This distribution is why blockchain is often called “trustless.” You don’t need to trust any single entity; the system itself ensures integrity.

Step 5: Transparency and Immutability

Blockchain records are public and permanent. Once a transaction is added, it’s there forever.

Let’s go back to our coffee analogy. Imagine writing your expense in a shared notebook. If you try to erase it later, everyone else will know because their copies don’t match. That’s the essence of blockchain’s immutability.

Use Cases: Beyond Bitcoin

Blockchain isn’t just about cryptocurrency. Its applications span industries:

- Supply Chain Management

- Track goods from origin to consumer.

- Verify authenticity (goodbye, fake Gucci bags).

- Healthcare

- Secure patient records.

- Improve drug traceability.

- Voting

- Prevent fraud.

- Ensure transparency.

- Real Estate

- Simplify property transfers.

- Eliminate middlemen.

Even NFTs (those quirky digital art pieces) rely on blockchain for authenticity.

Benefits of Blockchain

Why is everyone buzzing about blockchain? Here are the key perks:

1. Security

With its decentralized structure and cryptographic hashes, blockchain is incredibly hard to hack.

2. Transparency

Public ledgers mean anyone can verify transactions.

3. Efficiency

Automated processes reduce the need for intermediaries, saving time and money.

4. Accessibility

Anyone with an internet connection can participate in a blockchain network.

Challenges and Criticisms

Blockchain isn’t perfect. Here are some common critiques:

- Energy Consumption

- Proof of Work systems (like Bitcoin) consume massive amounts of electricity.

- Scalability

- Processing speed can slow as the network grows.

- Regulation

- Governments are still figuring out how to handle blockchain technology.

- Complexity

- It’s not user-friendly yet. Let’s face it—your grandma isn’t buying Bitcoin anytime soon.

Final Thoughts

So, how does blockchain work? At its simplest, it’s a decentralized, transparent, and secure way to record transactions. But peel back the layers, and it’s a technological marvel combining cryptography, consensus, and distribution.

The next time someone brings up blockchain at a party, you’ll have more to say than “Oh yeah, Bitcoin!” Whether it’s securing your finances, tracking your coffee beans, or creating the next digital Mona Lisa, blockchain is reshaping our world one block at a time.

What’s your take? Ready to dive into blockchain or still scratching your head?

Also Read: Predicting Crypto Prices for the 2025 Bull Run – BlockTech

Leave a Reply